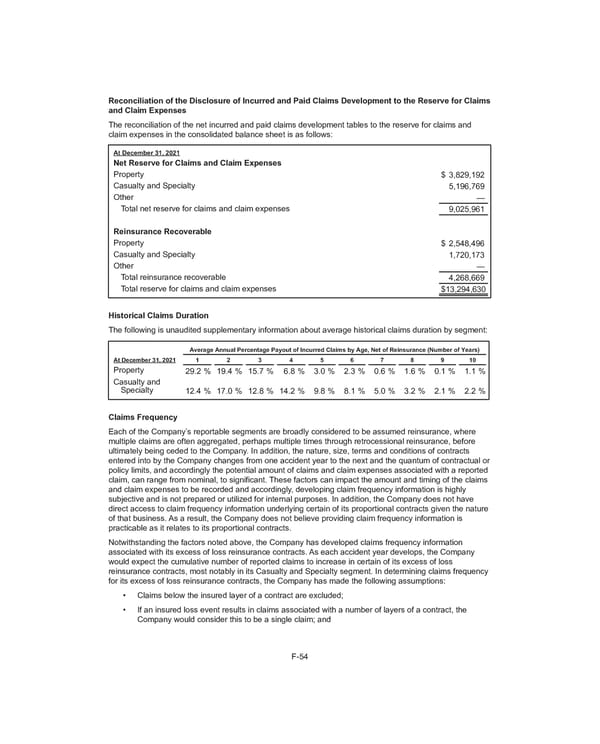

Reconciliation of the Disclosure of Incurred and Paid Claims Development to the Reserve for Claims and Claim Expenses The reconciliation of the net incurred and paid claims development tables to the reserve for claims and claim expenses in the consolidated balance sheet is as follows: At December 31, 2021 Net Reserve for Claims and Claim Expenses Property $ 3,829,192 Casualty and Specialty 5,196,769 Other — Total net reserve for claims and claim expenses 9,025,961 Reinsurance Recoverable Property $ 2,548,496 Casualty and Specialty 1,720,173 Other — Total reinsurance recoverable 4,268,669 Total reserve for claims and claim expenses $ 13,294,630 Historical Claims Duration The following is unaudited supplementary information about average historical claims duration by segment: Average Annual Percentage Payout of Incurred Claims by Age, Net of Reinsurance (Number of Years) At December 31, 2021 1 2 3 4 5 6 7 8 9 10 Property 29.2 % 19.4 % 15.7 % 6.8 % 3.0 % 2.3 % 0.6 % 1.6 % 0.1 % 1.1 % Casualty and Specialty 12.4 % 17.0 % 12.8 % 14.2 % 9.8 % 8.1 % 5.0 % 3.2 % 2.1 % 2.2 % Claims Frequency Each of the Company’s reportable segments are broadly considered to be assumed reinsurance, where multiple claims are often aggregated, perhaps multiple times through retrocessional reinsurance, before ultimately being ceded to the Company. In addition, the nature, size, terms and conditions of contracts entered into by the Company changes from one accident year to the next and the quantum of contractual or policy limits, and accordingly the potential amount of claims and claim expenses associated with a reported claim, can range from nominal, to significant. These factors can impact the amount and timing of the claims and claim expenses to be recorded and accordingly, developing claim frequency information is highly subjective and is not prepared or utilized for internal purposes. In addition, the Company does not have direct access to claim frequency information underlying certain of its proportional contracts given the nature of that business. As a result, the Company does not believe providing claim frequency information is practicable as it relates to its proportional contracts. Notwithstanding the factors noted above, the Company has developed claims frequency information associated with its excess of loss reinsurance contracts. As each accident year develops, the Company would expect the cumulative number of reported claims to increase in certain of its excess of loss reinsurance contracts, most notably in its Casualty and Specialty segment. In determining claims frequency for its excess of loss reinsurance contracts, the Company has made the following assumptions: • Claims below the insured layer of a contract are excluded; • If an insured loss event results in claims associated with a number of layers of a contract, the Company would consider this to be a single claim; and F-54

2021 Annual Report Page 196 Page 198

2021 Annual Report Page 196 Page 198