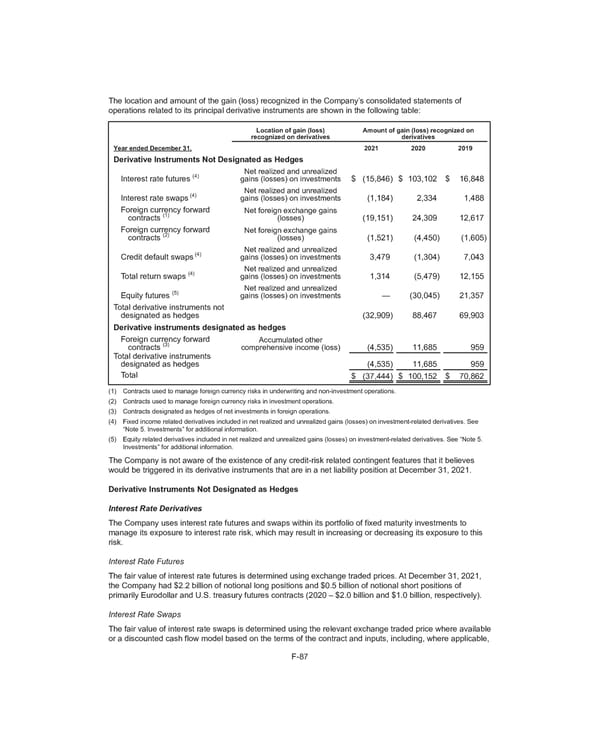

The location and amount of the gain (loss) recognized in the Company’s consolidated statements of operations related to its principal derivative instruments are shown in the following table: Location of gain (loss) recognized on derivatives Amount of gain (loss) recognized on derivatives Year ended December 31, 2021 2020 2019 Derivative Instruments Not Designated as Hedges Interest rate futures (4) Net realized and unrealized gains (losses) on investments $ (15,846) $ 103,102 $ 16,848 Interest rate swaps (4) Net realized and unrealized gains (losses) on investments (1,184) 2,334 1,488 Foreign currency forward contracts (1) Net foreign exchange gains (losses) (19,151) 24,309 12,617 Foreign currency forward contracts (2) Net foreign exchange gains (losses) (1,521) (4,450) (1,605) Credit default swaps (4) Net realized and unrealized gains (losses) on investments 3,479 (1,304) 7,043 Total return swaps (4) Net realized and unrealized gains (losses) on investments 1,314 (5,479) 12,155 Equity futures (5) Net realized and unrealized gains (losses) on investments — (30,045) 21,357 Total derivative instruments not designated as hedges (32,909) 88,467 69,903 Derivative instruments designated as hedges Foreign currency forward contracts (3) Accumulated other comprehensive income (loss) (4,535) 11,685 959 Total derivative instruments designated as hedges (4,535) 11,685 959 Total $ (37,444) $ 100,152 $ 70,862 (1) Contracts used to manage foreign currency risks in underwriting and non-investment operations. (2) Contracts used to manage foreign currency risks in investment operations . (3) Contracts designated as hedges of net investments in foreign operations. (4) Fixed income related derivatives included in net realized and unrealized gains (losses) on investment-related derivatives. See “Note 5. Investments” for additional information. (5) Equity related derivatives included in net realized and unrealized gains (losses) on investment-related derivatives. See “Note 5. Investments” for additional information. The Company is not aware of the existence of any credit-risk related contingent features that it believes would be triggered in its derivative instruments that are in a net liability position at December 31, 2021. Derivative Instruments Not Designated as Hedges Interest Rate Derivatives The Company uses interest rate futures and swaps within its portfolio of fixed maturity investments to manage its exposure to interest rate risk, which may result in increasing or decreasing its exposure to this risk. Interest Rate Futures The fair value of interest rate futures is determined using exchange traded prices. At December 31, 2021, the Company had $2.2 billion of notional long positions and $0.5 billion of notional short positions of primarily Eurodollar and U.S. treasury futures contracts (2020 – $2.0 billion and $1.0 billion, respectively). Interest Rate Swaps The fair value of interest rate swaps is determined using the relevant exchange traded price where available or a discounted cash flow model based on the terms of the contract and inputs, including, where applicable, F-87

2021 Annual Report Page 229 Page 231

2021 Annual Report Page 229 Page 231