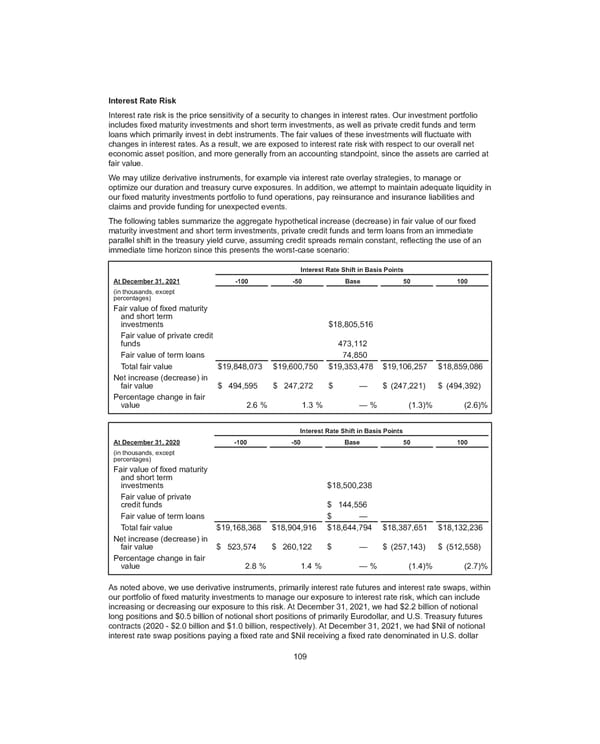

Interest Rate Risk Interest rate risk is the price sensitivity of a security to changes in interest rates. Our investment portfolio includes fixed maturity investments and short term investments, as well as private credit funds and term loans which primarily invest in debt instruments. The fair values of these investments will fluctuate with changes in interest rates. As a result, we are exposed to interest rate risk with respect to our overall net economic asset position, and more generally from an accounting standpoint, since the assets are carried at fair value. We may utilize derivative instruments, for example via interest rate overlay strategies, to manage or optimize our duration and treasury curve exposures. In addition, we attempt to maintain adequate liquidity in our fixed maturity investments portfolio to fund operations, pay reinsurance and insurance liabilities and claims and provide funding for unexpected events. The following tables summarize the aggregate hypothetical increase (decrease) in fair value of our fixed maturity investment and short term investments, private credit funds and term loans from an immediate parallel shift in the treasury yield curve, assuming credit spreads remain constant, reflecting the use of an immediate time horizon since this presents the worst-case scenario: Interest Rate Shift in Basis Points At December 31, 2021 -100 -50 Base 50 100 (in thousands, except percentages) Fair value of fixed maturity and short term investments $ 18,805,516 Fair value of private credit funds 473,112 Fair value of term loans 74,850 Total fair value $ 19,848,073 $ 19,600,750 $ 19,353,478 $ 19,106,257 $ 18,859,086 Net increase (decrease) in fair value $ 494,595 $ 247,272 $ — $ (247,221) $ (494,392) Percentage change in fair value 2.6 % 1.3 % — % (1.3) % (2.6) % Interest Rate Shift in Basis Points At December 31, 2020 -100 -50 Base 50 100 (in thousands, except percentages) Fair value of fixed maturity and short term investments $ 18,500,238 Fair value of private credit funds $ 144,556 Fair value of term loans $ — Total fair value $ 19,168,368 $ 18,904,916 $ 18,644,794 $ 18,387,651 $ 18,132,236 Net increase (decrease) in fair value $ 523,574 $ 260,122 $ — $ (257,143) $ (512,558) Percentage change in fair value 2.8 % 1.4 % — % (1.4) % (2.7) % As noted above, we use derivative instruments, primarily interest rate futures and interest rate swaps, within our portfolio of fixed maturity investments to manage our exposure to interest rate risk, which can include increasing or decreasing our exposure to this risk. At December 31, 2021, we had $2.2 billion of notional long positions and $0.5 billion of notional short positions of primarily Eurodollar, and U.S. Treasury futures contracts (2020 - $2.0 billion and $1.0 billion, respectively). At December 31, 2021, we had $Nil of notional interest rate swap positions paying a fixed rate and $Nil receiving a fixed rate denominated in U.S. dollar 109

2021 Annual Report Page 124 Page 126

2021 Annual Report Page 124 Page 126