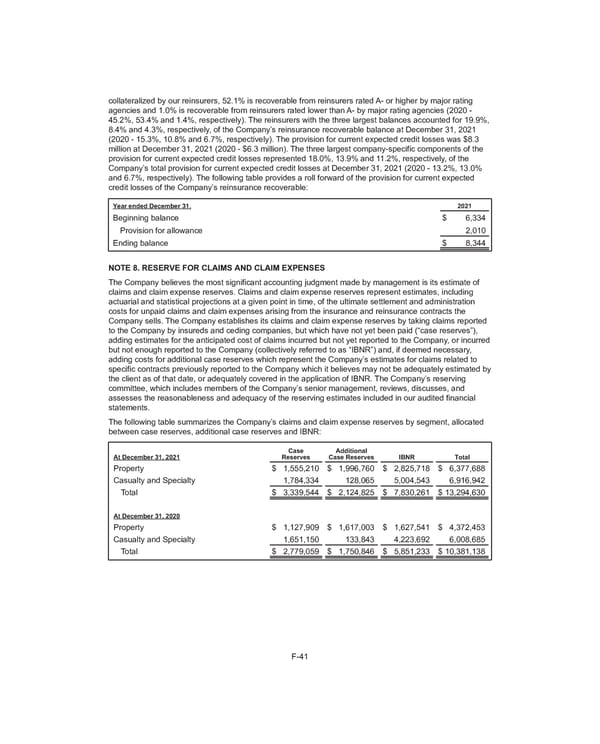

collateralized by our reinsurers, 52.1% is recoverable from reinsurers rated A- or higher by major rating agencies and 1.0% is recoverable from reinsurers rated lower than A- by major rating agencies (2020 - 45.2%, 53.4% and 1.4%, respectively). The reinsurers with the three largest balances accounted for 19.9%, 8.4% and 4.3%, respectively, of the Company’s reinsurance recoverable balance at December 31, 2021 (2020 - 15.3%, 10.8% and 6.7%, respectively). The provision for current expected credit losses was $8.3 million at December 31, 2021 ( 2020 - $6.3 million). The three largest company-specific components of the provision for current expected credit losses represented 18.0%, 13.9% and 11.2%, respectively, of the Company’s total provision for current expected credit losses at December 31, 2021 ( 2020 - 13.2%, 13.0% and 6.7%, respectively). The following table provides a roll forward of the provision for current expected credit losses of the Company’s reinsurance recoverable: Year ended December 31, 2021 Beginning balance $ 6,334 Provision for allowance 2,010 Ending balance $ 8,344 NOTE 8. RESERVE FOR CLAIMS AND CLAIM EXPENSES The Company believes the most significant accounting judgment made by management is its estimate of claims and claim expense reserves. Claims and claim expense reserves represent estimates, including actuarial and statistical projections at a given point in time, of the ultimate settlement and administration costs for unpaid claims and claim expenses arising from the insurance and reinsurance contracts the Company sells. The Company establishes its claims and claim expense reserves by taking claims reported to the Company by insureds and ceding companies, but which have not yet been paid (“case reserves”), adding estimates for the anticipated cost of claims incurred but not yet reported to the Company, or incurred but not enough reported to the Company (collectively referred to as “IBNR”) and, if deemed necessary, adding costs for additional case reserves which represent the Company’s estimates for claims related to specific contracts previously reported to the Company which it believes may not be adequately estimated by the client as of that date, or adequately covered in the application of IBNR. The Company’s reserving committee, which includes members of the Company’s senior management, reviews, discusses, and assesses the reasonableness and adequacy of the reserving estimates included in our audited financial statements. The following table summarizes the Company’s claims and claim expense reserves by segment, allocated between case reserves, additional case reserves and IBNR: At December 31, 2021 Case Reserves Additional Case Reserves IBNR Total Property $ 1,555,210 $ 1,996,760 $ 2,825,718 $ 6,377,688 Casualty and Specialty 1,784,334 128,065 5,004,543 6,916,942 Total $ 3,339,544 $ 2,124,825 $ 7,830,261 $ 13,294,630 At December 31, 2020 Property $ 1,127,909 $ 1,617,003 $ 1,627,541 $ 4,372,453 Casualty and Specialty 1,651,150 133,843 4,223,692 6,008,685 Total $ 2,779,059 $ 1,750,846 $ 5,851,233 $ 10,381,138 F-41

2021 Annual Report Page 183 Page 185

2021 Annual Report Page 183 Page 185