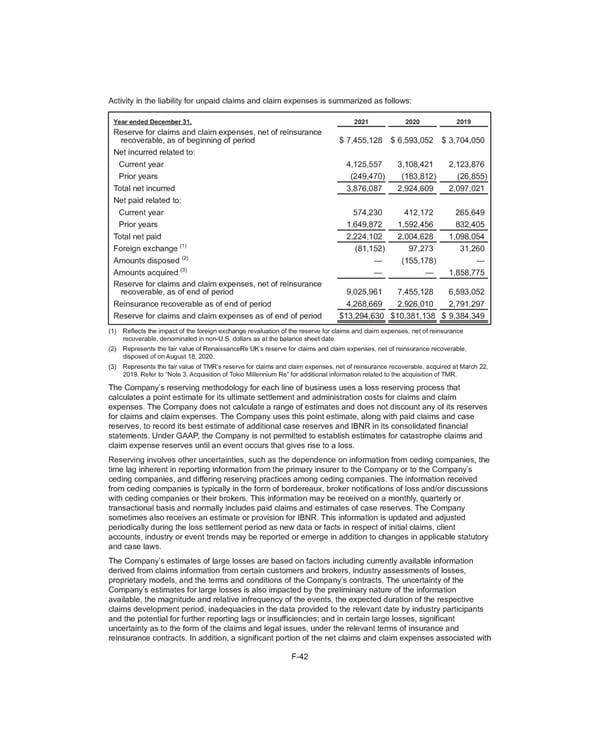

Activity in the liability for unpaid claims and claim expenses is summarized as follows: Year ended December 31, 2021 2020 2019 Reserve for claims and claim expenses, net of reinsurance recoverable, as of beginning of period $ 7,455,128 $ 6,593,052 $ 3,704,050 Net incurred related to: Current year 4,125,557 3,108,421 2,123,876 Prior years (249,470) (183,812) (26,855) Total net incurred 3,876,087 2,924,609 2,097,021 Net paid related to: Current year 574,230 412,172 265,649 Prior years 1,649,872 1,592,456 832,405 Total net paid 2,224,102 2,004,628 1,098,054 Foreign exchange (1) (81,152) 97,273 31,260 Amounts disposed (2) — (155,178) — Amounts acquired (3) — — 1,858,775 Reserve for claims and claim expenses, net of reinsurance recoverable, as of end of period 9,025,961 7,455,128 6,593,052 Reinsurance recoverable as of end of period 4,268,669 2,926,010 2,791,297 Reserve for claims and claim expenses as of end of period $ 13,294,630 $ 10,381,138 $ 9,384,349 (1) Reflects the impact of the foreign exchange revaluation of the reserve for claims and claim expenses, net of reinsurance recoverable, denominated in non-U.S. dollars as at the balance sheet date. (2) Represents the fair value of RenaissanceRe UK’s reserve for claims and claim expenses, net of reinsurance recoverable, disposed of on August 18, 2020. (3) Represents the fair value of TMR’s reserve for claims and claim expenses, net of reinsurance recoverable, acquired at March 22, 2019. Refer to “Note 3. Acquisition of Tokio Millennium Re” for additional information related to the acquisition of TMR. The Company’s reserving methodology for each line of business uses a loss reserving process that calculates a point estimate for its ultimate settlement and administration costs for claims and claim expenses. The Company does not calculate a range of estimates and does not discount any of its reserves for claims and claim expenses. The Company uses this point estimate, along with paid claims and case reserves, to record its best estimate of additional case reserves and IBNR in its consolidated financial statements. Under GAAP, the Company is not permitted to establish estimates for catastrophe claims and claim expense reserves until an event occurs that gives rise to a loss. Reserving involves other uncertainties, such as the dependence on information from ceding companies, the time lag inherent in reporting information from the primary insurer to the Company or to the Company’s ceding companies, and differing reserving practices among ceding companies. The information received from ceding companies is typically in the form of bordereaux, broker notifications of loss and/or discussions with ceding companies or their brokers. This information may be received on a monthly, quarterly or transactional basis and normally includes paid claims and estimates of case reserves. The Company sometimes also receives an estimate or provision for IBNR. This information is updated and adjusted periodically during the loss settlement period as new data or facts in respect of initial claims, client accounts, industry or event trends may be reported or emerge in addition to changes in applicable statutory and case laws. The Company’s estimates of large losses are based on factors including currently available information derived from claims information from certain customers and brokers, industry assessments of losses, proprietary models, and the terms and conditions of the Company’s contracts. The uncertainty of the Company’s estimates for large losses is also impacted by the preliminary nature of the information available, the magnitude and relative infrequency of the events, the expected duration of the respective claims development period, inadequacies in the data provided to the relevant date by industry participants and the potential for further reporting lags or insufficiencies; and in certain large losses, significant uncertainty as to the form of the claims and legal issues, under the relevant terms of insurance and reinsurance contracts. In addition, a significant portion of the net claims and claim expenses associated with F-42

2021 Annual Report Page 184 Page 186

2021 Annual Report Page 184 Page 186